IDFC Forex Card: Fees and Benefits

IDFC Forex Card offers zero issuance fees, multi-currency support, global acceptance, and enhanced security. Learn its benefits, fees, and how to apply.

IDFC Forex Card Fees & Benefits: What Every Trader Must Know

The IDFC FIRST Bank multi-currency forex card offers zero issuance and reload fees, making it a cost-effective choice for traders. It supports 14 currencies, provides real-time expense tracking, and includes free ATM withdrawals up to three times a month. Traders can avoid hidden charges by loading the right currencies and using the self-care portal to manage transactions efficiently. Whether you're a seasoned trader or just starting out in global markets, the IDFC Forex Card offers seamless financial transactions. If you're also looking into other trading tools, check out Traders Union's What is Exness Go guide for enhanced trading flexibility.

This article explores the key aspects of the IDFC Forex Card, including its features, fees, benefits, and application process. By understanding how it works, traders can make informed decisions and optimize their international transactions.

What is an IDFC Forex card and how does it work?

The IDFC FIRST Bank Multi-Currency Forex Card is a prepaid card that allows users to load multiple foreign currencies, enabling seamless international transactions without frequent currency conversions. It functions like a debit or credit card but is preloaded with foreign currencies, making it ideal for traders managing cross-border payments. Whether you're dealing with Euro to INR, AED to INR, or other exchange rates, this card helps in reducing conversion costs and making transactions smoother.

This card is especially beneficial for traders dealing with multiple currencies, as it eliminates the hassle of fluctuating exchange rates and the need for multiple bank accounts. Users can make purchases or withdraw cash in local currencies at VISA-supported merchants and ATMs worldwide, ensuring smooth transactions. For those following international market trends, platforms like Forex Factory can be useful in understanding forex fluctuations, helping traders make informed decisions about their currency holdings.

Additionally, the card enhances security by reducing the risks associated with carrying cash. It also provides real-time tracking through mobile banking, allowing traders to monitor expenses efficiently. Whether you are dealing with AUD to INR or SGD to INR, having a forex card that supports multiple currencies ensures that you are not affected by unnecessary conversion fees.

With its global acceptance, ease of use, and protection against currency fluctuations, the IDFC Forex Card is a reliable financial tool for international transactions, making it an excellent choice for frequent travelers and forex traders alike.

IDFC Forex card fees: A complete breakdown

Understanding the fee structure of the IDFC Forex Card is crucial for traders aiming to optimize their international transactions. Here's a detailed breakdown of the associated costs:

Issuance fee

IDFC FIRST Bank offers the Multi-Currency Forex Card with zero issuance charges, making it a cost-effective option for traders entering international markets. This fee waiver allows users to allocate more funds directly to their trading activities without incurring initial setup costs.

Reload fee

Traders can reload their Multi-Currency Forex Cards without any additional charges, providing flexibility in managing funds across various currencies. This feature is particularly advantageous for those who require frequent adjustments to their currency holdings, ensuring seamless operations without the concern of extra fees.

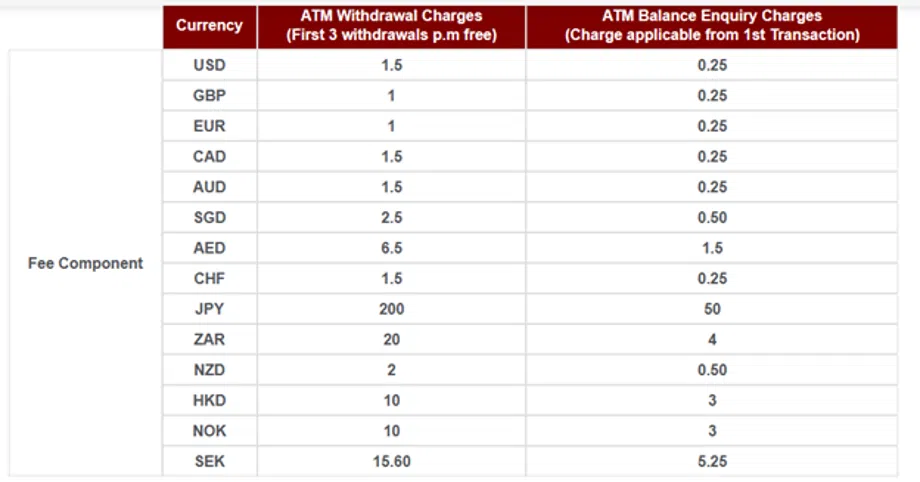

ATM withdrawal fee

The card grants global ATM access, with zero charges for the first three withdrawals each month. Subsequent withdrawals incur a fee of 1.5% per transaction. Being aware of these fees helps users plan their cash needs more effectively while abroad.

Currency conversion fee

For transactions conducted in currencies not preloaded onto the card, a cross-currency markup fee of 3.5% plus GST is imposed. This fee compensates for the currency conversion process. Users are advised to review the bank's terms and conditions regularly to stay informed about the applicable rates and make cost-effective decisions when dealing with multiple currencies.

Inactivity fee

An inactivity fee may be levied if the card remains unused for a specified period. To avoid this charge, it's advisable to use the card regularly or encash any remaining funds promptly after completing international transactions. Maintaining active use of the card ensures that traders do not incur unnecessary fees, thereby preserving their capital for trading purposes.

By familiarizing themselves with these fees, traders can effectively manage their expenses and utilize the IDFC FIRST Bank Multi-Currency Forex Card to its fullest potential in their international trading

Key benefits of using IDFC Forex card for traders

The IDFC Forex Card offers a plethora of advantages tailored to meet the needs of traders:

1. Cost efficiency

- Zero issuance and reload fees. Traders can acquire and reload the card without incurring additional charges, allowing more capital to be allocated directly to trading activities.

- Competitive exchange rates. The card provides favorable exchange rates, enabling traders to maximize their investments when dealing with multiple currencies.

2. Multi-currency support

- 14 supported currencies. The card supports 14 currencies, including USD, EUR, GBP, AUD, CAD, SGD, JPY, CHF, HKD, NZD, AED, CNH, NOK, and ZAR, allowing traders to manage funds across various markets seamlessly.

- Automatic wallet-to-wallet transfers. In case of insufficient funds in a particular currency, the card automatically transfers funds from another currency wallet, ensuring uninterrupted transactions.

3. Global accessibility

- Worldwide acceptance. The card is accepted at millions of visa merchant establishments and ATMs globally except in India, Nepal, and Bhutan, providing traders with the flexibility to conduct transactions wherever their business takes them.

- Single ATM PIN. A unified ATM PIN simplifies cash withdrawals across different countries, enhancing convenience for traders on the move.

4. Enhanced security

- Complimentary replacement card. Each card kit includes a free replacement card, ensuring that traders can quickly resume transactions in case of loss or damage to the primary card.

- Comprehensive travel insurance. The card offers best-in-class travel insurance coverage, providing financial protection against unforeseen events during international trading trips.

5. Efficient fund management

- Real-time expense tracking. Traders can monitor their spending in real-time through an intuitive self-service card management platform, facilitating better financial control.

- Free refund on return. Upon returning to India, traders can encash any unused balance on the card without additional fees, ensuring that funds are not unnecessarily tied up.

IDFC Forex card vs. other Forex cards: How it compares

Here's a detailed comparison of the IDFC FIRST Bank Multi-Currency Forex Card against other popular Forex cards

|

Feature |

IDFC FIRST Bank Forex Card |

BookMyForex Card |

HDFC Regalia ForexPlus Card |

SBI Multi-Currency Card |

|

Issuance & reload fees |

Zero |

Zero |

Rs. 500 issuance fee |

Rs. 100 + GST issuance fee |

|

ATM withdrawal fees |

Free for first 3 withdrawals, then 1.5% per transaction |

USD 2 per withdrawal |

Flat Rs. 125 per transaction |

Rs. 25 + GST per transaction |

|

Currency support |

14 currencies |

14 currencies |

20+ currencies |

7 currencies |

|

Cross-currency fees |

3.5% + GST |

3.5% + GST |

Zero |

3.5% + GST |

|

Global acceptance |

Accepted worldwide (except India, Nepal, Bhutan) |

Widely accepted |

Accepted globally |

Accepted globally |

|

Replacement card |

Free spare card included |

Chargeable |

Chargeable |

Not included |

|

Expense tracking |

Real-time tracking via mobile app |

Available via app |

Mobile app support |

Limited tracking options |

|

Travel insurance |

Included |

Limited coverage |

Included |

Limited coverage |

How to apply for an IDFC Forex card: Step-by-step guide

Applying for the IDFC FIRST Bank multi-currency forex card is a straightforward process designed for individuals traveling internationally. Here is a step-by-step guide to applying both online and offline.

1. Eligibility criteria

Before applying, ensure you meet the following requirements.

- Account holder. You must have an active savings account with IDFC FIRST Bank.

- Purpose of travel. The card is intended for individuals traveling abroad for education, business, or leisure.

2. Required documentation

Prepare the necessary documents for a smooth application process.

- Valid passport. A copy of your current passport.

- A copy of the visa for your destination country.

- Air ticket. A copy of your confirmed flight ticket.

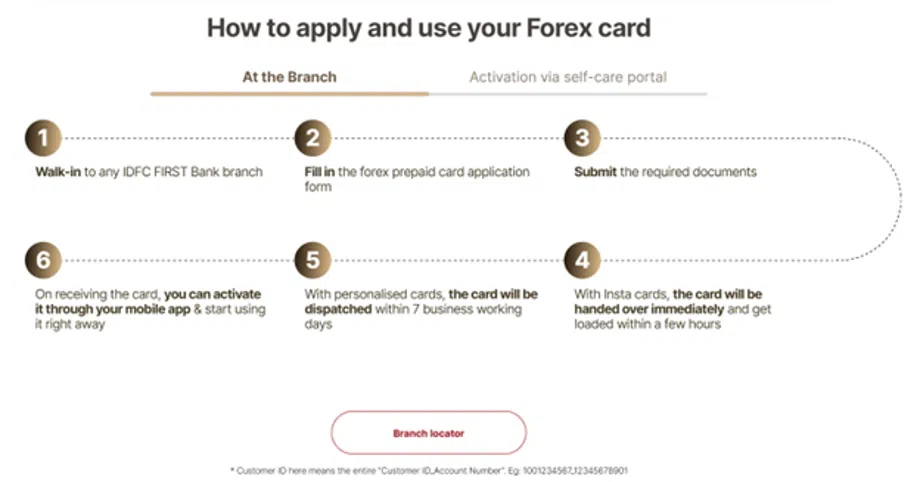

3. Application methods

You can apply for the forex card either online through the self-care portal or by visiting a branch in person.

A. Online application via self-care portal

- Access the portal. Visit the IDFC FIRST Bank self-care portal.

- Login credentials. Enter your registered mobile number or customer ID.

- Set password. If accessing for the first time, set a new password using the OTP sent to your registered mobile number.

- Activate card. Once logged in, select 'activate card' to initiate the activation process.

- Set/reset PIN. Choose 'manual PIN set/reset' to establish your card's PIN.

- Preferences setup. Navigate to 'preferences' to configure channel preferences and set daily transaction limits.

B. Offline application at a branch

- Locate a branch. Find the nearest IDFC FIRST Bank branch.

- Visit the branch. Carry the required documents to the branch.

- Application form. Fill out the forex card application form available at the branch.

- Submit documents. Provide copies of your passport, visa, and air ticket along with the completed form.

- Card issuance.

- Insta card. Issued immediately and can be loaded within a few hours.

- Personalized card. Dispatched within seven business days.

- Card activation. Activate your card through the IDFC FIRST Bank mobile app or self-care portal.

4. Activation and usage

- Use the self-care portal or mobile app to activate your card and set your PIN.

- Loading funds. Transfer the desired amount in supported currencies to your forex card.

- Managing preferences. Set transaction limits and channel preferences through the self-care portal.

5. Additional information

- Zero issuance and reload fees. The IDFC FIRST Bank forex card has no issuance or reload charges, making it cost-effective for international travelers.

- Global acceptance. The card is accepted at millions of visa merchant establishments and ATMs worldwide, excluding India, Nepal, and Bhutan.

- Security features. Equipped with chip and PIN technology, the card ensures enhanced security for transactions.

Tips to maximize savings & avoid hidden charges

Maximizing savings and avoiding hidden charges with your IDFC FIRST Bank multi-currency forex card requires strategic planning and informed usage. Here are some insightful tips to help you make the most of your card.

1. Understand the fee structure

- Issuance and reload fees. The IDFC FIRST Bank forex card has zero charges on issuance, loading, and reloading, making it a cost-effective choice for international travelers.

- ATM withdrawal fees. The first three ATM withdrawals each month are free. After that, a 1.5% fee per transaction applies. Plan your cash needs to minimize withdrawal frequency and avoid unnecessary charges.

- Cross-currency charges. Transactions in currencies not preloaded on your card incur a 5% plus GST markup fee. To avoid this, load your card with the specific currencies of the countries you plan to visit.

2. Monitor merchant category codes (MCC)

- Hidden charges alert. Some transactions may attract unexpected charges due to their MCC classification. Certain merchants process payments under utility or other categories, leading to additional forex fees.

- Verify before large payments. Always check the MCC classification with the merchant before making large purchases to avoid surprise charges.

3. Avoid dynamic currency conversion (DCC)

- Always pay in local currency. Merchants may offer to charge your card in your home currency instead of the local currency. This process, known as dynamic currency conversion (DCC), results in poor exchange rates and extra fees.

- Decline DCC at checkout. Always choose the local currency when making international purchases to secure better rates and avoid unnecessary markups.

4. Use the self-care portal for expense control

- Set transaction limits. Adjust daily spending and withdrawal limits to avoid overspending and enhance security.

- Monitor transactions in real-time. Regularly review your transaction history through the self-care portal to detect unauthorized charges.

- Lock/unlock card instantly. If your card is lost or stolen, you can instantly lock it through the portal to prevent misuse.

5. Consider alternative cards for specific needs

- IDFC FIRST WOW! credit card. This FD-backed card offers zero forex markup fees, 4X reward points on international transactions, and interest-free ATM withdrawals for up to 48 days.

- IDFC FIRST Mayura credit card. Provides zero forex markup and an interest-free period on cash withdrawals, making it ideal for frequent travelers.

6. Monitor exchange rates before loading funds

- Exchange rates fluctuate daily. Keep an eye on forex rates and load your card when rates are most favorable.

- Use currency alerts. Some forex tracking apps allow you to set alerts when a currency reaches your preferred exchange rate.

7. Be mindful of inactivity fees

- Use your card regularly. Some forex cards charge inactivity fees if unused for a prolonged period.

- Encash leftover funds. If you don't plan to use the card soon, withdraw or transfer the balance back to your account to avoid potential fees.

IDFC Forex Card offers a range of benefits for travelers and forex users

According to the insights of financial analyst Ivan Andriyenko, the IDFC Forex Card offers a range of benefits for travelers and forex users, making it a competitive option in the market. This card is designed to provide convenience, security, and cost-effectiveness for international transactions, helping users manage their expenses efficiently while traveling abroad.

One of the key advantages of the IDFC Forex Card is its low foreign exchange markup fees, which make international transactions more affordable compared to traditional credit or debit cards. Additionally, the card supports multiple currencies, allowing users to load and spend in different countries without worrying about fluctuating exchange rates or additional conversion fees.

Security is another crucial factor, as forex cards are safer than carrying cash. The IDFC Forex Card comes with EMV chip protection and features like instant blocking in case of loss or theft, ensuring enhanced security for users. Furthermore, with zero forex markup on select transactions, the card helps travelers save significantly on cross-border payments.

From a usability perspective, the IDFC Forex Card is widely accepted across international ATMs, POS terminals, and online merchants, making it a reliable payment option during travel. Additionally, it allows for easy reloading, ensuring travelers can manage their funds without disruptions.

According to Kharitonov, while the IDFC Forex Card provides excellent benefits, users should carefully review the fee structure, reload charges, and withdrawal costs to maximize savings. Comparing forex cards based on individual travel needs and spending patterns is essential to choosing the best option. Overall, the IDFC Forex Card stands out as a cost-efficient, secure, and user-friendly alternative for those looking to manage foreign currency transactions with ease.

Conclusion

The IDFC FIRST Bank Multi-Currency Forex Card is a reliable and cost-effective solution for traders handling international transactions. With zero issuance and reload fees, CHIP & PIN security, global acceptance, and comprehensive insurance, it simplifies cross-border payments while minimizing financial risks. By allowing multiple currencies on a single card, traders can efficiently manage expenses across different markets without frequent currency conversions.

To make the most of this forex card, traders should understand its fee structure, benefits, and application process. Regular usage, monitoring exchange rates, and staying informed about potential charges can help maximize savings.

FAQs

What are the fees associated with the IDFC Forex Card?

The fees vary based on usage, but some common charges include issuance fees, reload fees, ATM withdrawal fees, and inactivity fees. However, IDFC often provides competitive pricing, making it one of the cost-effective forex cards in the market.

How does the forex markup fee work on the IDFC Forex Card?

A forex markup fee is a charge applied when making transactions in a currency that is not preloaded onto the card. IDFC Forex Card offers zero forex markup on select currencies, ensuring cost savings for travelers using the supported currency wallets.

Is the IDFC Forex Card better than using a credit or debit card for international transactions?

Yes, in many cases. Unlike credit or debit cards that charge high foreign exchange conversion fees (usually 3-5%), the IDFC Forex Card provides fixed exchange rates, lower forex markup, and reduced withdrawal fees, making it a more economical choice for travelers.

Can the IDFC Forex Card be reloaded while traveling?

Yes, the card can be reloaded online through the IDFC FIRST Bank portal or mobile app, making it convenient for travelers who need additional funds while abroad.

About the Author

This article was written by Maxim Nechiporenko, a financial expert and author at Traders Union. With a career in media dating back to 2006, he has extensive knowledge in finance, investment, and geoeconomics. Maxim focuses on delivering timely insights into trading, cryptocurrencies, and financial markets, helping investors navigate the industry with clear analysis, reviews, and expert guidance.

(Disclaimer: Devdiscourse's journalists were not involved in the production of this article. The facts and opinions appearing in the article do not reflect the views of Devdiscourse and Devdiscourse does not claim any responsibility for the same.)